You pull up your credit report and spot it immediately: an account you never opened, a late payment marked on a bill you paid on time, or a balance that's just plain wrong. Your score is taking a hit for something that isn't even accurate. You've heard that a "credit repair letter" can fix this, but you're not sure what that actually means or whether it's just another promise that won't deliver. The good news is that credit repair letters can genuinely work, but only when you use them correctly, for the right reasons, and with the right documentation behind them.

Table of Contents

- Understanding what credit repair letters can (and cannot) do

- Preparing to write: what you need before sending a letter

- Step-by-step: how to write an effective credit repair letter

- What happens next: timelines, outcomes, and follow-up

- Other letter types: goodwill letters and pay-for-delete explained

- Our take: the smart path for real credit repair

- Need more help? Explore our credit improvement solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Only errors can be removed | Credit repair letters only work to remove or correct inaccurate or incomplete information, not valid negatives. |

| Be specific and organized | Clearly identify errors, provide evidence, and keep organized records to increase your chance of success. |

| Follow proper steps | Send your dispute to each bureau reporting the error using the recommended structure and certified mail. |

| Expect realistic results | Dispute investigations usually take up to 30 days and result in corrections, not guaranteed score boosts. |

| Other letters have limits | Goodwill and pay-for-delete letters may work in some cases, but outcomes are never guaranteed. |

Understanding what credit repair letters can (and cannot) do

Before you write a single word, you need to understand the boundaries. Credit repair letters are not magic wands. They are legal tools, and like any tool, they only work when applied to the right job.

The most important thing to know is this: accurate negative information generally cannot be removed from your credit report through disputes. If you genuinely missed three payments last year, no letter will erase that. The CFPB is clear on this point, and any service promising otherwise is misleading you.

What credit repair letters can legitimately accomplish is significant, though. Here is what falls within their realistic scope:

- Correcting mixed files: Sometimes your report contains information from someone with a similar name or Social Security number. That is a real error and fully disputable.

- Fixing wrong balances or dates: A creditor may report an incorrect balance or a wrong date of first delinquency. These are correctable.

- Removing identity theft entries: If someone opened accounts in your name, you have strong grounds to dispute those items.

- Challenging unverifiable items: If a creditor cannot verify a reported item, bureaus must remove it if it cannot be confirmed as accurate.

- Correcting incomplete information: An account reported as "in collections" that was actually settled is incomplete and worth disputing.

"You generally cannot have negative information removed from your credit report if it is accurate." — Consumer Financial Protection Bureau

This matters because the credit repair industry is full of misleading services that charge hundreds of dollars to send letters that will never produce results for accurate negative entries. Knowing the difference protects your time and your money.

Preparing to write: what you need before sending a letter

Setting realistic expectations is step one. Step two is gathering your materials. A well-prepared dispute letter is far more effective than a vague complaint. Bureaus and creditors respond better when you give them specific, organized evidence.

Start by pulling your credit reports from all three major bureaus. You can access free reports at AnnualCreditReport.com. Review each one carefully because errors may appear on one bureau's report but not another. This is also why you should send disputes separately to each bureau rather than sending one letter and hoping it covers everything.

Here is a checklist of what you need before you write:

- A copy of your full credit report with the disputed item clearly circled or highlighted

- Copies (never originals) of supporting documents such as bank statements, payment confirmations, court records, or identity theft reports

- Your full legal name, current address, date of birth, and Social Security number for identification

- The name of the creditor, account number, and the specific error you are disputing

- A clear, one or two sentence explanation of why the information is wrong

| Document type | Purpose | Notes |

|---|---|---|

| Credit report copy | Identify and mark disputed items | Circle or highlight each error |

| Bank statements | Prove on-time payments | Match dates to disputed entries |

| Payment receipts | Confirm settled accounts | Include confirmation numbers |

| Identity theft report | Support fraud-related disputes | File at IdentityTheft.gov first |

| Correspondence copies | Show prior contact with creditor | Useful for follow-up disputes |

Pro Tip: Organize your documents in the same order you reference them in your letter. This makes it easier for the investigator reviewing your dispute to match your claims to your evidence quickly, which can speed up the process.

Once you have everything organized, you are ready to write. Do not rush this step. A disorganized dispute with vague claims is far less likely to succeed than a focused, well-documented one.

Step-by-step: how to write an effective credit repair letter

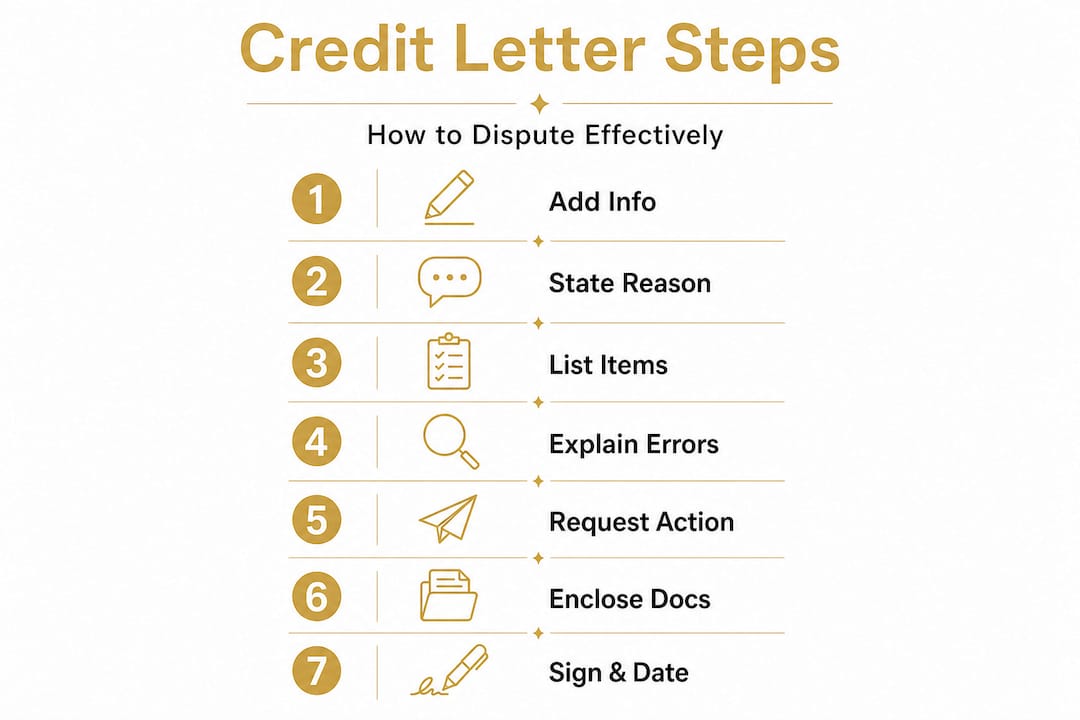

The structure of your letter matters as much as its content. Bureaus process thousands of disputes. A clear, professional letter that follows a logical format gets taken seriously. Here is how to build one that works.

1. Start with your identifying information. At the top of the letter, include your full name, current address, date of birth, and the last four digits of your Social Security number. This helps the bureau match your letter to your file without confusion.

2. State the purpose immediately. In the first paragraph, clearly state that you are writing to dispute specific items on your credit report. Do not bury the lead. Be direct.

3. List each disputed item specifically. For every error you are disputing, include the creditor name, account number, and the exact nature of the error. For example: "Account #XXXX with ABC Bank is reported as 60 days late on March 2024. I made this payment on time, and I have enclosed a bank statement confirming the transaction date."

4. Explain why each item is inaccurate. One sentence per item is usually enough. Be factual, not emotional. Stick to the facts.

5. State what you want. Ask for the item to be corrected or removed. The FTC sample letter recommends explicitly requesting removal or correction and enclosing supporting documentation. Do not leave it ambiguous.

6. List your enclosures. At the end of the letter, list every document you are including. This creates a paper trail and confirms what you submitted.

7. Sign and date the letter. Include a handwritten signature if sending by mail.

| Letter element | What to include | Common mistake to avoid |

|---|---|---|

| Identifying info | Name, address, DOB, SSN last 4 | Leaving out account numbers |

| Disputed item | Creditor, account #, error type | Being vague or general |

| Reason for dispute | One clear factual sentence | Writing emotional narratives |

| Requested action | Delete or correct | Not stating what you want |

| Enclosures | List every document | Sending originals instead of copies |

Send your letter by USPS certified mail with return receipt requested. This gives you a legal timestamp proving when the bureau received your dispute, which is important if you need to follow up or escalate.

Pro Tip: Keep a complete copy of everything you send, including the letter, all enclosures, and the certified mail receipt. This file becomes your evidence if the bureau fails to respond within the required timeframe.

What happens next: timelines, outcomes, and follow-up

You have sent your letter. Now you wait, but not passively. Understanding the timeline keeps you informed and ready to act if something goes wrong.

Credit reporting companies are generally required to investigate disputes within 30 days of receiving your dispute. In some cases, such as when you submit additional relevant information during the investigation, that window can extend to 45 days.

| Stage | Timeframe | What happens |

|---|---|---|

| Bureau receives letter | Day 1 | Investigation clock starts |

| Bureau contacts furnisher | Within a few days | Creditor asked to verify the item |

| Investigation period | Up to 30 days (45 in some cases) | Bureau reviews evidence from both sides |

| Results sent to you | Within 5 days of completion | Written notice of outcome |

| Report updated | Immediately after decision | Corrected or removed if dispute upheld |

Here is what to watch for in the outcome:

- Dispute upheld: The item is corrected or removed. Your score may improve after the next reporting cycle.

- Dispute denied: The bureau found the information to be accurate. You can ask for a statement of dispute to be added to your file, which notes that you contest the item.

- No response: If the bureau fails to investigate within the required timeframe, you have the right to escalate to the CFPB or consult a consumer protection attorney.

One important reality check: if an item is accurate but negative, it will stay on your report for a set period regardless of any letters you send. Most negative information stays for seven years, and bankruptcy information remains for up to ten years. The goal of a dispute letter is correction, not permanent erasure of valid history.

Statistic to know: Studies and consumer advocacy groups consistently note that one in five Americans has an error on at least one of their credit reports. That means millions of people have legitimate grounds to dispute something right now.

Other letter types: goodwill letters and pay-for-delete explained

Beyond formal disputes, there are two other letter strategies worth knowing about. Neither carries the legal weight of an FCRA (Fair Credit Reporting Act) dispute, but they are worth understanding.

Goodwill letters are written directly to a creditor asking them to remove a negative item as a gesture of goodwill, usually because you have an otherwise strong payment history and the negative entry was a one-time mistake. There is no legal obligation for the creditor to comply, and results vary widely based on the creditor, the account history, and how you frame your request.

Pay-for-delete letters are a negotiation tactic where you offer to pay a collection account in exchange for the collector removing the entry from your report. This sounds appealing, but it comes with real caveats.

- Not all collectors will agree to pay-for-delete arrangements

- Even if they agree verbally, get it in writing before you pay

- Accurate information may still remain on your report even after payment, depending on the creditor's policies

- Some credit scoring models factor in paid collections differently than unpaid ones, so paying can still help your score even without deletion

Goodwill and pay-for-delete letters are not guaranteed strategies. They are conversations, not legal rights. Use them as supplementary tools, not primary solutions.

The most honest advice here is to treat these options as worth trying in the right circumstances, but do not count on them. Your energy is better spent on accurate, documented disputes for genuine errors first.

Our take: the smart path for real credit repair

Here is something most articles won't say directly: the people who get the best results from credit repair are not the ones who find the cleverest loophole. They are the ones who understand exactly what the law allows, document everything, and stay consistent.

We have seen readers spend hundreds of dollars on "credit repair services" that sent the same generic dispute letters to all three bureaus, with no supporting documentation and no follow-up strategy. The results were predictably poor. Not because credit repair letters do not work, but because those letters were not built on evidence.

The law is actually on your side when you have a legitimate error. The FCRA gives you real rights: the right to dispute, the right to a timely investigation, and the right to have unverifiable information removed. That is powerful. But those rights only activate when you use them correctly.

Patience is also part of the process. Credit repair is not a one-week fix. It is a series of deliberate actions over weeks and months. Tracking your disputes, following up on time, and monitoring your reports after corrections are what separate people who see real score improvements from those who stay frustrated.

The shortcut mentality is what the scammers exploit. When you know the actual process, you do not need shortcuts. You just need a plan, the right documents, and the discipline to follow through.

Need more help? Explore our credit improvement solutions

If you have read this guide and feel ready to take action, that is exactly where you want to be. But sometimes having a clear starting point and the right tools makes all the difference between getting started and getting stuck.

At Lifestyle LLC, we have built resources specifically for people who are serious about repairing their credit and building real financial momentum. Whether you are dealing with your first dispute or managing a more complex credit situation, our credit improvement tools are designed to support you at every stage. You do not have to figure this out alone. The right guidance, combined with your own effort and documentation, is what produces lasting results.

Frequently asked questions

How often can I send a credit repair letter to dispute the same error?

You can submit a new dispute if you have new information or additional documentation to support your claim, but disputing without new facts may cause the bureau to label it as frivolous and decline to investigate.

Will my credit score improve immediately after a successful dispute?

If an error is corrected or removed, your score can improve, but the change typically appears after the next reporting cycle, not right away. The investigation process itself can take up to 30 days before any update is reflected.

Can accurate but negative information be removed through a credit repair letter?

No. Accurate negative information cannot be legally removed from your credit report before it naturally ages off, regardless of what any letter says.

How long do negative items stay on my credit report if valid?

Most negative information stays for seven years, and bankruptcy information remains for up to ten years as long as it is accurate.

What documentation should I send with my credit dispute letter?

Include a copy of your credit report with the disputed items circled, copies of supporting documents like bank statements or payment confirmations, and keep all originals for your own records. The FTC recommends never sending original documents, only copies.